Over the past twelve months, the market for high bandwidth memory has evolved from a specialist segment for high-end accelerators to a system-critical bottleneck for the entire AI industry. HBM no longer only determines the performance data of individual chips, but also the actual deliverability of complete platforms. Anyone who is unable to deliver here will be dropped from roadmaps, regardless of how good their GPU or accelerator architecture looks on paper. Against this backdrop, the development at Samsung should be read less as a short-term market movement and more as a necessary strategic self-correction after a phase in which the Group had visibly lost ground in its own core business.

At the beginning of 2025, it became apparent that Samsung’s HBM strategy was suffering from several simultaneous pressures. The switch to higher stack complexity, increasing data rates and stricter thermal conditions was met with a market that no longer showed any tolerance for unstable deliveries or inconsistent quality. HBM is no longer a classic memory product, but a highly integrated component of complex packages in which DRAM die, interposers, substrates and packaging processes must function as a unit. Even small deviations in yield, timing or thermal behavior are enough to delay or completely lose qualifications. During this phase, Samsung was unable to translate its nominal DRAM capacity into corresponding HBM volumes, which led directly to a loss of market share.

The decisive turning point did not come from a single new product generation, but from a visible shift in internal priorities. Instead of maximizing capacity, the focus shifted to process stability, and instead of aggressive ramp-ups, to more conservative but reproducible production. This is often invisible to the market, but is immediately noticeable to customers. HBM customers not only evaluate peak bandwidth or pin speed, but above all the ability of a supplier to maintain identical quality windows over months. The moment Samsung was able to meet this expectation again, the Group gradually returned to relevant supply chains.

HBM3E played the role of a technological hinge. This generation is sophisticated enough to mercilessly expose weak manufacturing processes, but at the same time still close enough to existing platforms to enable wider adoption. The fact that Samsung has been able to regain a foothold here indicates that key problems with yield stability, thermal characterization and signal integrity have at least been solved to the extent that customers can once again expect predictable quantities. This also explains why market shares have visibly shifted over the course of the year, without this being accompanied by spectacular product announcements.

Looking ahead, HBM4 is increasingly coming into focus, albeit less as a pure speed record and more as a stress test for a manufacturer’s overall industrial performance. Higher data rates not only mean faster interfaces, but also more stringent requirements for power delivery, package design and system integration. At the same time, the market remains structurally undersupplied, which politicizes pricing and turns supply contracts into strategic instruments. Samsung is signaling significantly greater flexibility here than a year ago, which indicates that market presence and long-term platform loyalty are currently given higher priority than short-term margin optimization.

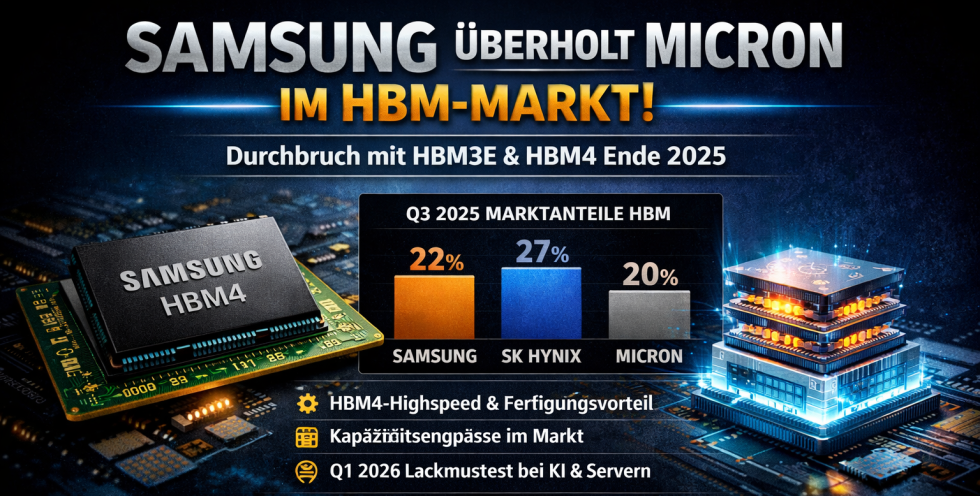

The fact that Samsung is now ahead of a direct competitor again is relevant in this context, but not an end point. Market shares in the HBM segment are volatile because they depend heavily on individual platform launches, ramp timings and delivery commitments. Sustainability will only come about when several generations are passed through without new breaks and customers not only test HBM, but firmly plan it into their roadmaps. The real benchmark will therefore not be a single quarter, but the phase from the beginning of 2026, when HBM4 will be integrated into productive AI systems on a larger scale.

Until then, it should be noted that Samsung’s current position should be seen less as a triumph and more as a return to competition. The company has shown that it is able to address structural weaknesses and regain lost ground. Whether this results in a lasting shift in the balance of power depends less on marketing or roadmaps than on the unspectacular but crucial question of how stable, scalable and reliable the company’s own production really is on a day-to-day basis. This is precisely where everything is now decided in the HBM market.

| Source | Key message | Link to |

|---|---|---|

| Wccftech | Samsung has increased its HBM market share again after sluggish quarters thanks to HBM3E and HBM4 breakthroughs. | https://wccftech.com/the-tables-are-turning-for-samsung-in-the-hbm-market/ |

| Chosun Biz | Samsung achieved ~22% HBM market share in Q3 2025, overtaking Micron according to Counterpoint Research. | https://biz.chosun.com/en/en-it/2025/12/19/PAW7TLJHIFF3NPCUSZF2CZBIOE/ |

| Futu News | Counterpoint data shows Samsung achieved more HBM sales in 2025 than Micron in the same period. | https://news.futunn.com/en/post/66427735/institution-samsung-s-hbm-revenue-to-surpass-micron-s |

| Counterpoint Research | Industry data on DRAM/HBM shares and trends with focus on Samsung’s recovery in the memory segment. | https://germany.counterpointresearch.com/insights/samsung-erobert-im-dritten-quartal-2025-spitzenposition-auf-dem-globalen-speichermarkt-zuruck/ |

Bisher keine Kommentare

Kommentar

Lade neue Kommentare

Artikel-Butler

Alle Kommentare lesen unter igor´sLAB Community →